There's a phrase making the rounds in every AI-in-finance presentation right now: "autonomous finance." It sounds like a destination — a future state where AI runs your finance function and humans step back. It conjures images of empty offices and software doing the month-end close while the CFO plays golf.

That's not what it means. And the misunderstanding matters, because the real version of autonomous finance is probably closer than most owners assume — and the things standing in the way aren't what the vendors are selling against.

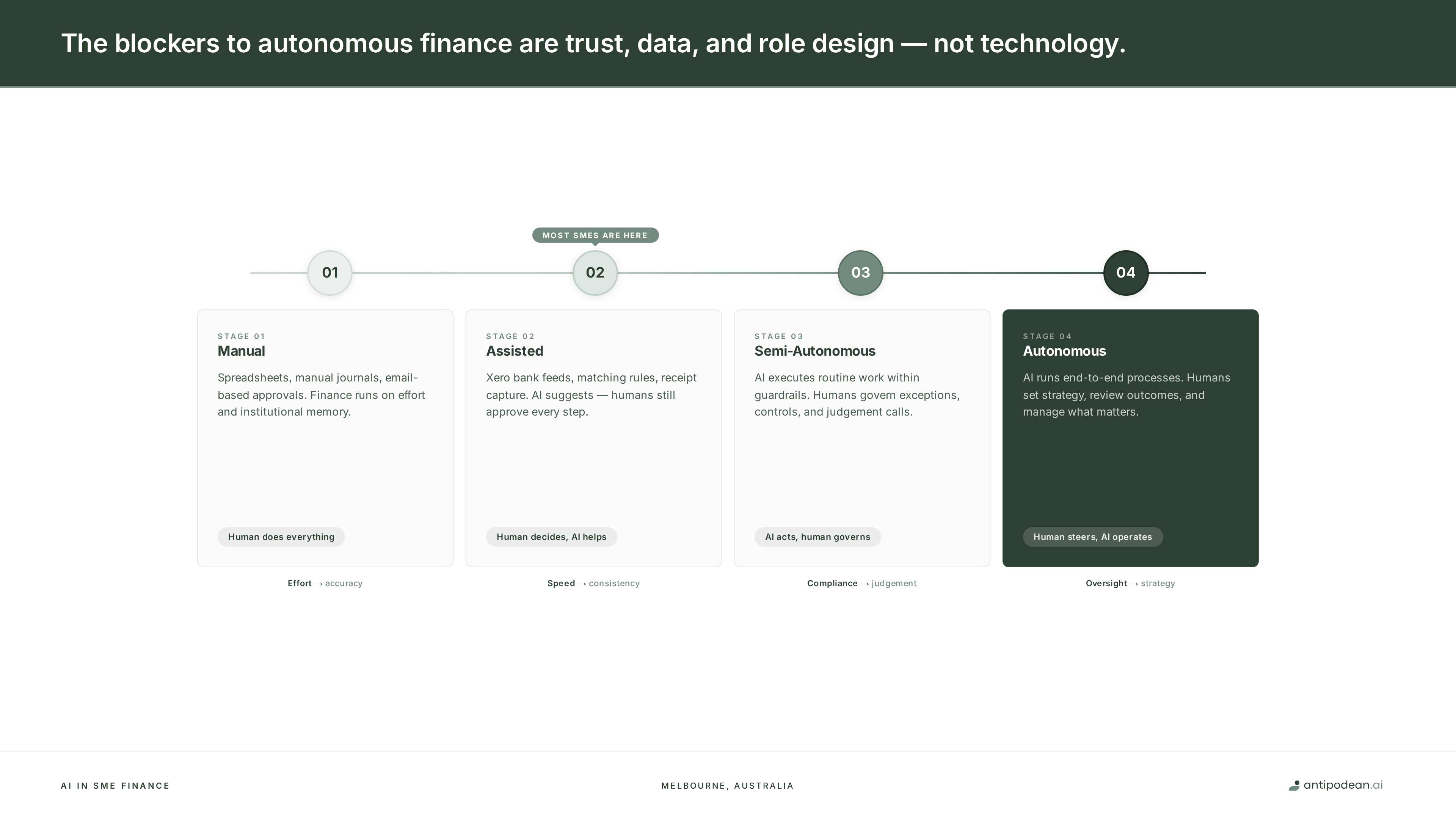

What autonomous finance actually means

Let's be precise. Autonomous finance doesn't mean unattended finance. It means a finance function where AI handles more of the execution layer — transactions, reconciliation, routine reporting, standard journals — and humans shift toward governance, exceptions, and decisions. The machine does more of the repetitive work. The human sets the rules, reviews the outcomes, and manages the edge cases. That's the direction, at least. How far any individual business gets depends on a few things.

If you're running a $5–30 million professional services business, this matters more than it might seem at first glance. Your finance team is probably two to five people. They're spending the majority of their time on data processing, not data analysis. Month-end takes a week. Forecasting is quarterly at best. The CFO or finance lead is buried in transactions when they should be in the room helping the business make decisions.

Autonomous finance — to the degree it's achievable — doesn't replace that team. It restructures what they spend their time on.

Where most businesses actually sit

We work with SME finance teams every week, and the pattern is remarkably consistent. Almost every business running Xero or a cloud accounting platform is at Stage 02 — Assisted. Bank feeds run automatically. Receipt capture works. Matching rules catch most transactions. AI is present in the system, but humans still approve every single step.

That's not a bad place to be. It's a massive improvement over manual accounting. But it's also a plateau. The productivity gain from Stage 01 to Stage 02 was obvious — you could see it in the hours saved. The gain from Stage 02 to Stage 03 is harder to see, because it's not about speed. It's about what your people spend their time on.

That matches what we see on the ground. Most finance functions are either experimenting with AI or haven't started. The technology has moved faster than adoption — but that gap exists for reasons that are worth understanding, not dismissing.

The three real blockers

If the technology for autonomous finance broadly exists — and it largely does, with caveats — why aren't more businesses moving? It's rarely about budget. It's three things that don't appear in vendor pitch decks:

1. Trust

Finance is the most risk-averse function in any business. It should be. The numbers flow into tax returns, loan covenants, board reports, and investor updates. A mistake isn't a bug — it's a compliance exposure.

This makes finance leaders inherently cautious about handing control to AI. And the caution is justified — AI still hallucinates, still misclassifies, still makes errors that a competent bookkeeper would catch immediately. That's not a problem to be solved by next quarter's software update. It's a structural limitation of how these tools work right now. The path forward isn't to ignore that. It's to build trust incrementally: let the AI do the work, but audit the output. Start with low-stakes processes. Expand the scope only as confidence — based on evidence, not marketing — grows.

2. Data quality

AI can only be as good as the data it works with. And honestly, for most SMEs, the data is a bit of a mess. That's fine when a bookkeeper is interpreting it — humans are good at reading context, recognising patterns, and working around inconsistencies. But autonomous systems aren't. They need clean, structured, consistent data to operate without constant human correction. And most businesses aren't there yet.

This is the most underestimated blocker. It's not glamorous. Nobody writes LinkedIn posts about cleaning up their chart of accounts. But it's probably the single biggest determinant of whether AI can move from suggesting to executing. A business with clean, well-coded data in Xero has a realistic path. One running on a patchwork of legacy categories and manual workarounds does not — regardless of what tool it buys.

3. Role design

This is the one nobody talks about. If AI takes over more of the transaction processing, what does your finance team actually do? In theory, the answer is governance, exceptions, analysis, business partnering. In practice, most teams haven't been set up for that shift.

Most finance job descriptions still read like they were written in 2015. Data entry, reconciliation, report preparation, compliance filing. These are execution tasks. If AI takes on more of that execution — and that's a genuine "if," not a certainty — the human role needs to shift toward oversight, judgement, and strategic input. That requires different skills, different metrics, and a different way of thinking about what the finance function is for. And that kind of change doesn't happen by installing a new tool.

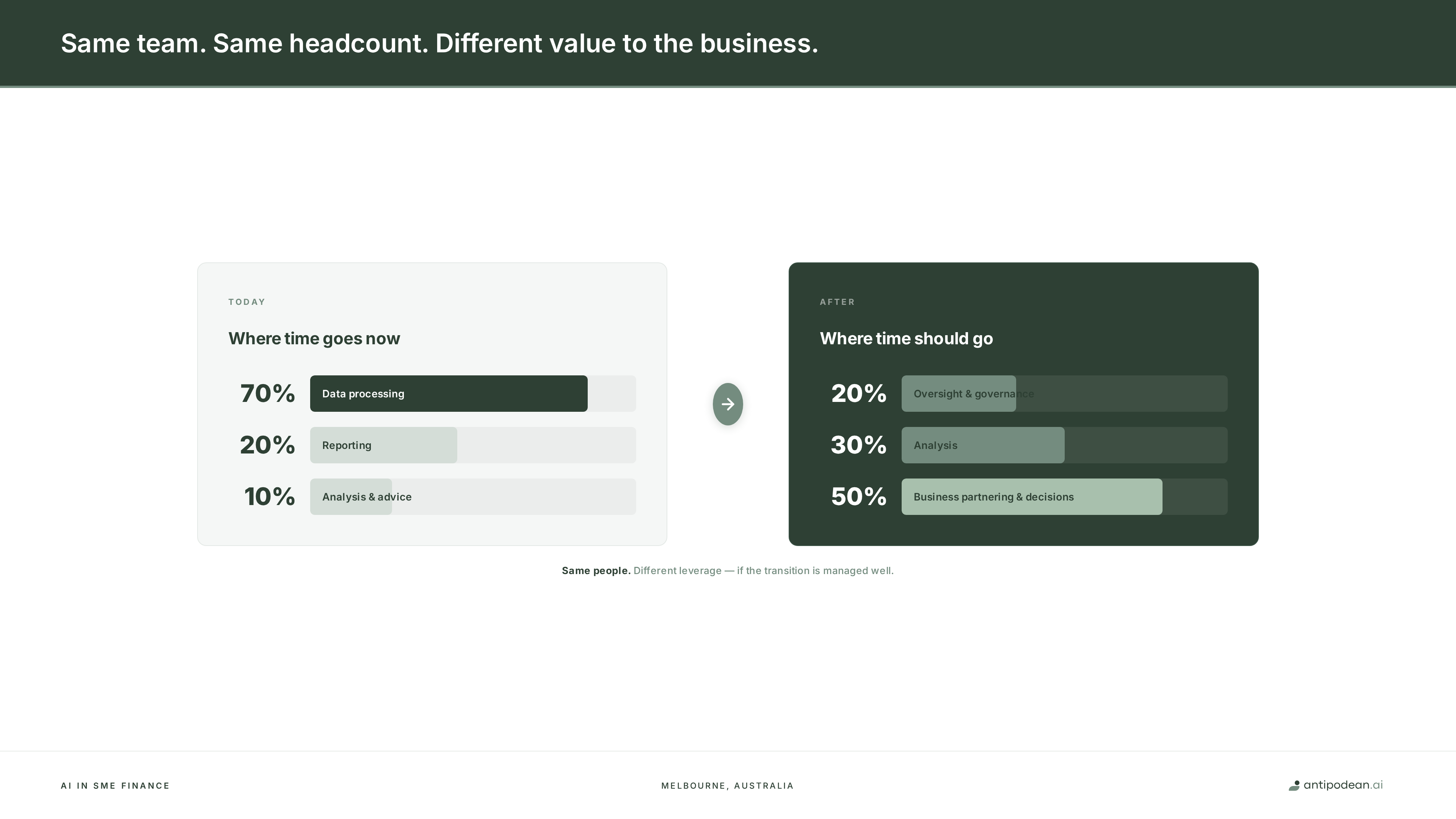

Before: Finance team spends 70% of time on data processing, 20% on reporting, 10% on analysis and advice.

After: Finance team spends 20% on oversight and governance, 30% on analysis, 50% on business partnering and decision support.

Same team. Same headcount. Potentially very different value to the business — if the transition is managed well.

Why this matters for professional services businesses

If you're running a law firm, accounting practice, consulting business, or engineering firm at $5–30 million in revenue, you probably have a small finance team that punches well above its weight. They're running payroll, managing WIP, reconciling trust accounts, preparing BAS returns, and trying to produce something resembling a forward view — all at the same time.

These are the businesses where the shift toward semi-autonomous finance could have the highest leverage. Not because the savings are the largest in dollar terms, but because the time freed up has the highest opportunity cost. When your finance lead spends less time reconciling bank accounts and more time modelling the impact of a new hire or a pricing change, the business potentially makes better decisions. That's the trade-off worth pursuing.

Professional services firms also tend to have simpler data than product businesses — fewer SKUs, simpler supply chains, more predictable revenue patterns. That doesn't mean the data is clean, but it does mean the cleanup is usually more manageable. The path from Stage 02 to Stage 03 is likely shorter for a services business than for a manufacturer or retailer — which is worth knowing if you're trying to decide whether this is worth the effort.

The practical path forward

If you're a business owner reading this and thinking "this sounds right but I don't know where to start" — you're not alone. Here's a practical sequence that we think makes sense for most SMEs:

Months 1–3: Foundation. Clean up your chart of accounts. Standardise naming conventions, remove duplicates, archive unused codes. Get your data into a state where a machine can read it consistently. This is probably the highest-leverage work most businesses can do, and it costs almost nothing.

Months 4–9: Controlled autonomy. Identify two or three processes where AI can execute with human review — bank reconciliation, invoice matching, receipt coding. Let the system run, but audit every output for three months. Build the trust through evidence, not faith.

Months 10–18: Role redesign. As AI handles more execution, deliberately shift your finance team's time toward analysis, forecasting, and business partnering. Update job descriptions. Change the metrics you use to evaluate the function. The finance team's value should be measured in decisions influenced, not transactions processed.

None of this requires new headcount. None of it requires a six-figure technology investment. It requires clarity about what your finance function is for, and a willingness to work through the blockers — which are real, but not insurmountable.

The fully autonomous finance function is still some way off for most businesses. But the meaningful shift — from assisted to semi-autonomous, where AI handles more of the routine and your team focuses more on decisions — is a realistic goal for a well-run SME. It takes time, clean data, and honest assessment of where you actually are. The technology is broadly ready. The harder question is whether the business is willing to do the unglamorous work to get there.

Want to map out what autonomous finance looks like for your business?

Book a free 15-minute call. No pitch, just an honest conversation about where you are and what to try next.

Book a Call →